About this study and M&BD Consulting

Based in French-speaking Switzerland, the cradle of luxury watchmaking, strategic consulting firm M&BD Consulting conducted a unique and comprehensive study in 2023 on the current and future challenges of the sector. The firm's experience within the Swiss economic fabric, along with various missions carried out in the luxury sector, led it to explore this fascinating topic more closely with a fresh and external view. The study is based on an analysis of over 300 documents, interviews with more than 50 industry leaders and the collection of expectations and opinions from over 400 watch buyers. It was conducted in partnership with GMT Publishing and WorldTempus.

A decisive period for the industry

Luxury watchmaking is at a pivotal moment in its existence. This unique industry composed of both family businesses and major groups is currently facing numerous development opportunities. The potential is there, the indicators are green. The watchmaking industry has experienced remarkable growth until the fall of 2023 in terms of both production and sales. The total value of Swiss watch exports reached record levels in 2023, with a growth rate of 7.7% registered from January to November compared to 2022 (FH, 2023). Market-leading brands achieved very good results, testifying to their unwavering expansion. In addition, the number of people working in the sector also increased, growing by over 7% between 2022 and 2023 (CPIH, 2023).

Numerous challenges to overcome

Although the luxury watchmaking sector is performing well, it is facing numerous challenges. Indeed, the sustained growth of recent years is showing signs of slowing down. Both in terms of new products exports and secondary market prices - a new indicator of the sector's health - the period of unbridled expansion seems to be levelling off.

Rising energy, labour, and raw material costs, as well as various geopolitical conflicts are disrupting the production schedules of watch companies and their subcontractors. These costs further increase the prices of timepieces which were already on the rise due to brands' pricing strategies, damping the purchasing desire of buyers whose acquisition capacity is also diminishing.

In addition to these economic challenges, there are many structural challenges. Developing the right distribution strategy, exploiting the secondary market potential, addressing staff shortages, promoting diversity in a conservative environment, positioning oneself in the face of market premiumization, and successfully attracting young and female customers are just some of the issues that industry leaders need to address.

Distribution: which strategy to adopt?

Choosing the most suitable distribution strategy considering the constraints imposed by the different channels is one of the most important challenges faced by watch brands today and in the years to come. Whether to develop a network of retailers, open new mono-brand stores, or invest in an online sales platform, the decisions are complex and require careful consideration.

The trend is towards mono-brand boutiques

A trend towards "mono-brand" strategies appears to be emerging among watch companies which have the necessary resources. Indeed, several players such as Audemars Piguet, TAG Heuer, Omega and IWC have opened new mono-brand boutiques in recent years (Sell-Out Index, Mercury Project, 2022). Moreover, many have chosen to restrict their network of retailers, as have some of the brands mentioned previously.

Selling timepieces directly offers many advantages. It allows brands to get closer to their customers, to better understand their expectations and needs, and to regain access to customer data. Direct selling also enables companies to generate higher profit margins, regain control over customer experience, control the selling price of watches, and offer a wider range of the brand's collections.

However, even for desirable brands able to attract customers on their own, opening brand-owned boutiques involves numerous challenges. It requires significant financial investment to gain access to high-visibility locations. Additionally, selling requires specific skills and knowledge that differ from producing. Moreover, it exposes the brand to greater risks during difficult periods.

Retailers have not said their last word

Working with a network of retailers is far from uninteresting for brands. Their local roots and in-depth knowledge of regional clientele foster personal relationships and informed sales. Their varied offerings attract a wider customer base willing to compare different brands and allow companies to benefit from “passing” clientele. Moreover, the withdrawal of certain players can benefit other brands, whether emerging or smaller, which do not have the resources to open mono-brand stores.

The inevitable e-commerce

In addition to the two distribution channels mentioned above, e-commerce is also gaining ground. Once overlooked by sector players, the share of online sales is growing and represents between 5% and 10% for some brands today. Driven by the pandemic, the shopping habits of younger customers, and the secondary market, the growth of digital is prompting many brands to invest significant resources in their digital channels.

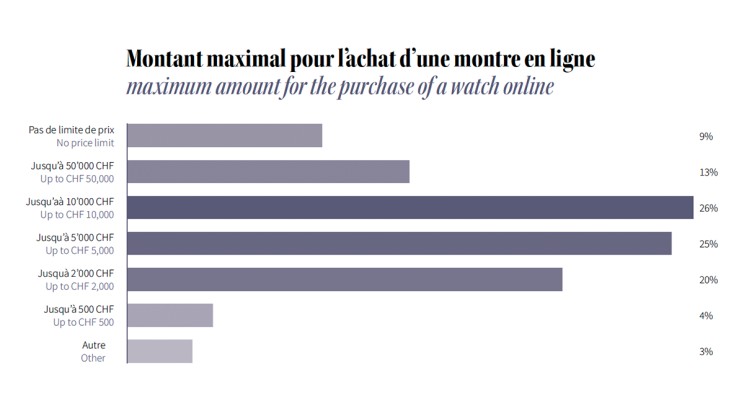

According to the results of our survey of hundreds of luxury watch buyers, 57% of participants would be "willing to buy a watch online". And the amounts they are willing to spend can be substantial: 25% of respondents would be willing to buy a watch online for up to CHF 5,000, 26% up to CHF 10,000, and 13% up to CHF 50,000.

And even if some market players interviewed do not perceive significant sales potential through digital channels, it has become an essential and unavoidable touchpoint in the purchasing process, particularly for information gathering that directly influences the final purchase.

Read the full study

In our comprehensive study, we address many other themes such as the industry's position on the challenges of certification, security, and digitalization, the identification of different categories of buyers, the expectations and opinions of over 400 watch purchasers, the results of a “mystery shopper” tour in nearly 30 mono-brand and multi-brand boutiques in Geneva, and the latest key market figures.

Discover the full Luxury Watchmaking Study, and for more info contact: info@mbdconsulting.ch